introduction

The Federal Budget is focused on increasing support for housing development to address the current housing crisis, by introducing over $6.2 billion in new and additional spending on social and affordable housing, new housing infrastructure and rent assistance.

However, from a tax perspective, the Federal Budget provided little stimulus to increase investment in the sector. While we expect the announced measures will have an impact on housing additions, we urge the Government to undertake further consultation with industry on the previously announced Build to Rental (BTR) tax incentives. The original exposure draft legislation falls short in a number of key areas and these need to be addressed if we are to achieve the expected 150,000 apartment additions over the next decade (as modelled by the Real Estate Institute of Australia).

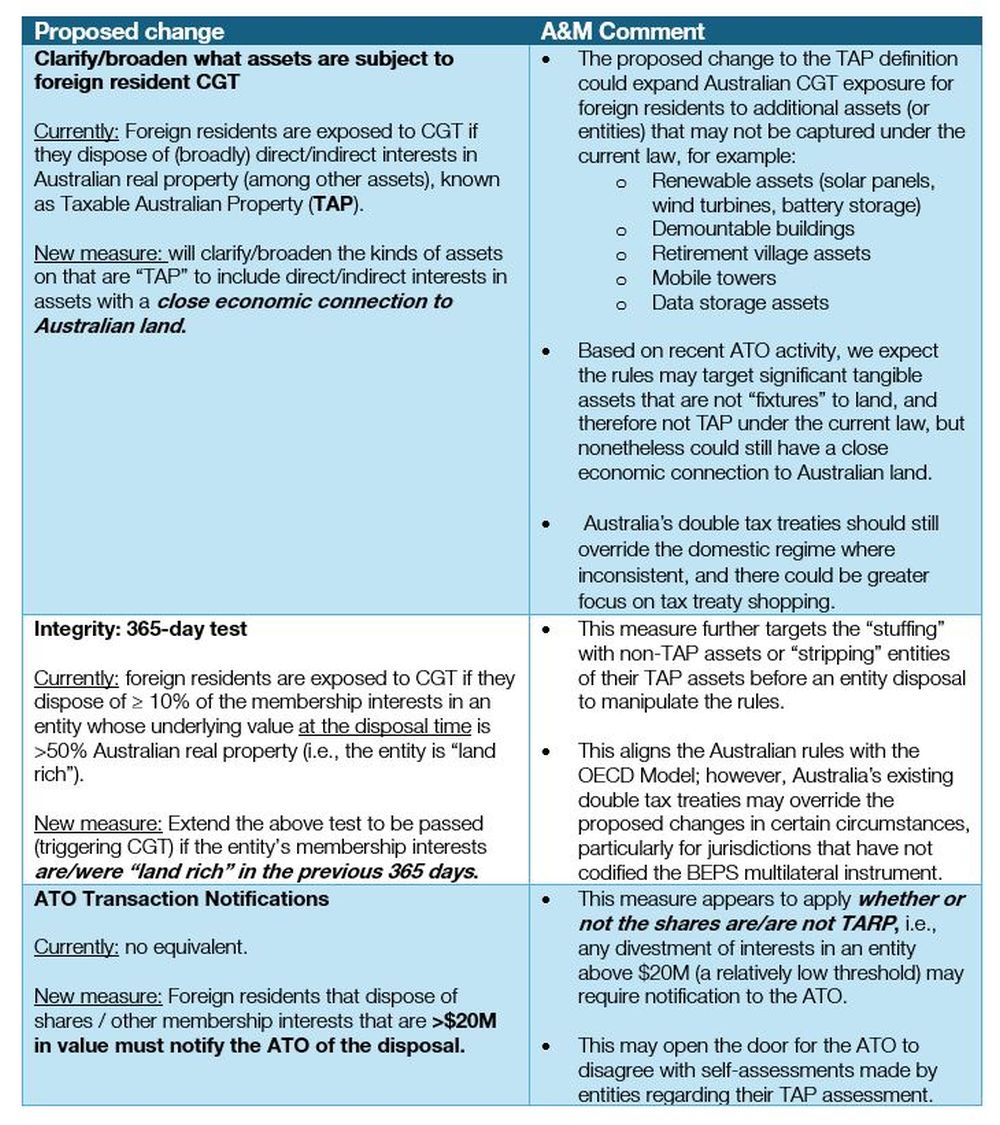

Strengthening the Capital Gains Tax (CGT) regime for expatriates

Among the most significant corporate tax changes, the Federal Budget announced new changes to the expatriate capital gains tax regime aimed at expanding and clarifying these rules, with the Treasury Department projecting that implementation will increase tax on expatriate investors by $200 million per year ($600 million in total).

The Federal Budget announcement stated that consultation will take place to allow affected businesses to have a say in any complex issues that may arise as these changes are implemented, and A&M will be contributing to these discussions.

Starting July 1, 2025, three changes are scheduled to come into effect:

Other relevant federal budget measures

International Financial Committee

The Budget reaffirms previously announced and welcomed changes to Australia's foreign investment framework, including:

- Refund 75% of fees for foreign investment applications that did not proceed because they failed to win competitive bidding.

- Allowing foreign investors to acquire existing BTR properties (provided the properties continue to be operated as BTR developments)

- A reduction in FIRB fees for BTR properties (provided the property continues to be operated as a BTR development).

In our view, the impact of the BTR changes will depend on the final shape of the BTR tax incentives.

PBSA

More detail has been provided about the role universities will play in addressing the housing shortage. It confirms that universities will have regulatory requirements to provide new purpose-built student accommodation (PBSA) to increase international student enrolments beyond their initial allocations. New PBSA must be available to both local and international students. Universities will be required to partner with external PBSA developers and operators to meet these requirements. Providers are encouraged to engage with universities early to ensure they can involve universities in the consultation process.

Thin capitalization

Unfortunately, the Federal Budget confirmed that recent changes to the thin capitalisation regime have only exempted Australian plantation entities from the revenue-based test. Industry groups are calling for Australian real estate entities to also be exempt from the new thin capitalisation rules, given that these rules pose a challenge to stimulating investment in Australian housing by foreign resident investors.

First published on May 19, 2024

The content of this article is intended to provide a general guide on the subject matter. Professional advice should be sought regarding specific circumstances.